Enterprises Embrace Converged Systems

The box counters at IDC are still working on a method to dice and slice how the market for converged systems is shaping up. Last year, as it was clear that machines that preconfigure servers, storage, networks, and management software – and sometimes all the way up to systems software preconfigured for very specific workloads. Up until now, some of this software was not counting in IDC’s model, but with the statistics that IDC has released for 2013, this software is now included.

IDC carves up what we at EnterpriseTech call converged systems into two different submarkets. Integrated Infrastructure systems are machines that have servers, storage, and networking, but they are not tuned up for specific workloads and are not configured with specific system and application software. Integrated Platform systems, on the other hand, are often based on similar server, storage, and networking components, all pre-integrated and pre-tested, but they are tuned to run a specific application and they usually include that application (although sometimes not in the base sticker price for the hardware).

The important thing, as far as enterprise customers are concerned, is that vendors have created these two types of machines to help speed their time to market with new applications and their peers seem to be taking a shining to them in specific cases. It looks like the systems market is splitting into three pieces – those who will keep buying the way they have been doing, those who want these converged systems, and those who are going for the kinds of barebones, distributed server and storage clusters with parallel applications that are exemplified by the Googles and Facebooks and Yahoos of the world. There are, of course, many tens of millions of companies worldwide who buy tower machines or a modest rack or two of servers and storage, and they drive plenty of volumes. But in the aggregate, they only drive something on the order of the same volumes as the top several hundred hyperscale customers. (Think about that for a second, and then ponder what happens if SMBs just throw in the towel and move to public clouds.)

Add up the two pieces of this integrated systems market, and IDC now reckons, with the addition of the software stacks to the platform side of the business, that these customers bought a very respectable 2.4 exabytes of storage capacity (generally a mix of disk with a dash of flash) for all of 2013, which was up 78.6 percent compared to storage shipments in 2012. The overall external disk storage market, by contrast, was growing at around 25 percent per year as 2013 was coming to a close and accounts for over 40 exabytes of capacity.

(IDC did not indicate how many server nodes or switches are embedded in these integrated infrastructure and integrated platform setups. It would be nice if it did so, of course.) The server market has seen shipments grow modestly in 2013, but revenues have been sluggish as hyperscale companies and cloud builders drag down average selling prices and virtualization (both in private datacenters and in public clouds) continues to drive up efficiencies, allowing companies to buy a lot less excess capacity.

In any event, IDC believes total revenues for integrated systems reckons that all told, these machines accounted for $7.66 billion in revenues for 2013 (that’s infrastructure plus platforms together), an increase of 45.6 percent compared to sales in 2012.

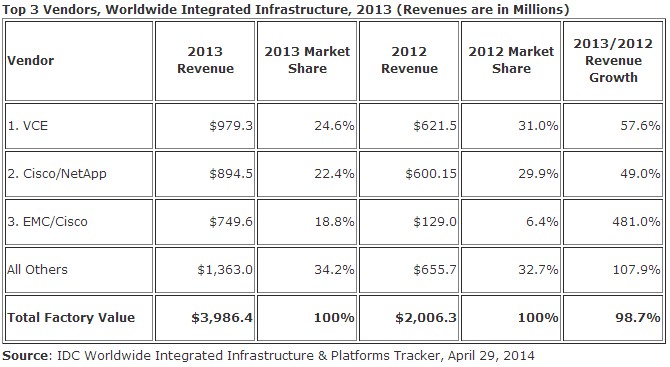

The real growth came from sales of integrated infrastructure systems, which nearly doubled in 2013, to just under $4 billion in aggregate sales across all vendors who are peddling such gear. And all of the top tier system makers are doing just that, as are a slew of upstarts who are trying to make money off the integration and simplicity play. Here is how IDC ranks the top vendors:

The Virtual Compute Environment partnership between EMC, Cisco Systems, and VMware tops the list with its Vblock setups, and the FlexPod systems created by NetApp and Cisco came in second with the VSPEX machines sold by EMC and Cisco (separately from the VCE alliance) came in third. If you are sensing a theme here, it is that Cisco, which more or less created this converged system category when it launched its Unified Computing System platform five years ago, has come to dominate this integrated infrastructure play from the server and switch perspective. The EMC-Cisco machines not sold under the VCE partnership just exploded in 2013. Oddly enough, Cisco’s revenue share of the pie went down from 67.3 percent to 65.8 percent as IBM, Hewlett-Packard, and Dell ramped up sales of their respective PureSystems, CloudSystem, and Active System converged machines and grew just a little bit faster. Still, that is precisely the kind of market share that Cisco historically likes. Cisco does not, however, make anywhere near the 65 percent margins it does in switching and routing in the UCS business, as the company’s executives admitted to EnterpriseTech at the five year anniversary of the UCS launch.

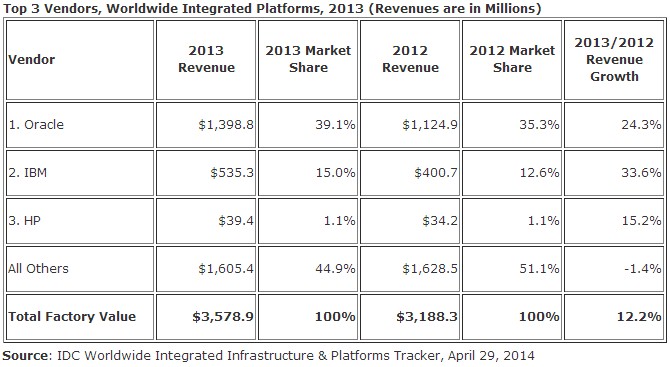

On the integrated platforms side of this market, software giant and systems player Oracle dominates with its Exadata, Exalogic, Exalytics, and Sparc SuperCluster machines. Here’s how IDC stacks and racks the players:

As you can see, there is a lot of variety in this market still, but all of the Others (and you can probably put HP in that category considering how small its revenue stream from integrated platforms was in 2013) are only getting a smattering of business from each supplier. It is hard to say what this means. It is hard to believe that several dozen companies peddling what amount to appliances can survive on a few tens of millions of dollars each in revenues each year. Markets tend to consolidate, and these Others are already seeing some slippage from 2012 to 2013, according to the IDC data in the table above.

VCE said in a separate statement that it had a goal of exiting 2013 with an annualized run rate of sales (bookings to be specific, not revenues) for Vblock systems, and in fact the company hit a $1.8 billion level for all products and services relating to the Vblock systems. The company added that in the first quarter of this year ended in March, demand was up more than 50 percent and marking the fourth consecutive quarter of growth. VCE has sold more than 1,750 Vblock systems (that is cluster configurations, not individual UCS enclosures) to more than 800 customers since it started peddling machines three years ago. HP has sold CloudSystems and AppSystems to more than 1,000 customers, but doesn't talk about system counts. IBM counts enclosures and says it has sold more than 10,000 to its PureSystems customers (including infrastructure and platform types, to use IDC's naming conventions). Cisco has said that there are close to 30,000 customers using UCS iron in its many flavors.

IDC reckons that the integrated infrastructure part of the converged systems market will swell at a compound annual growth rate of 43.2 percent, rising from $3.6 billion in 2013 to $11.2 billion in 2017.