The Rise Of Server Upstarts

The battle between the tier one incumbent server makers and Cisco Systems and the custom server makers continued in the first quarter of the year, and the upstarts are gaining ground on both the shipment and revenue fronts.

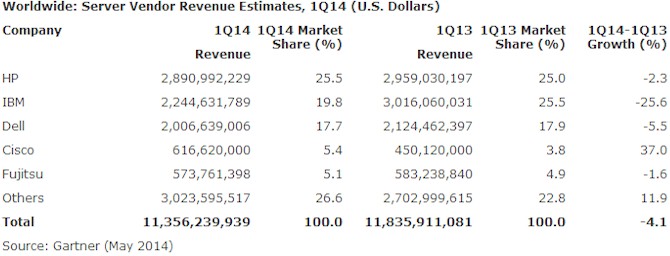

During the three months that ended in March, Gartner reckons that the world consumed 2.36 million servers, an increase of 1.4 percent over the prior year's first quarter. These machines, however, generated only $11.36 billion in revenues, down 4.1 percent year-on-year. Some of the revenue decline is due to the slippage in the Unix market, which is dominated by RISC and Itanium systems that are coming down in price and that are being displaced by Linux and Windows systems. Unix-based machines still added up to $1.19 billion in revenues in the quarter, a decline of 16.9 percent. The normal tailing off of mainframe sales towards the middle of a System z product cycle, where it is at right now, also put a damper on revenues in Q1. If you look at X86 servers alone, this architecture accounted for all but a few hundred thousand machines, with shipments rising 1.7 percent to 2.34 million, and revenues up 2.8 percent to $9.37 billion.

As might be expected given the pending $2.3 billion acquisition of the System x division by Lenovo, IBM's X86 server business had a tough quarter, with steep declines in both revenues and shipments. IBM has been clear that the entire System x division will be moving over to Lenovo should the deal be approved by regulators, and told EnterpriseTech last week that the deal was on track to close before the end of the year. It is not clear how IBM's many thousands of enterprise customers feel about the deal, but the statistics from Gartner certainly show a massive slowdown, with revenues for Big Blue down 25.6 percent to $2.24 billion and shipments down 27.8 percent to 166,311 units.

"There is no doubt that some IBM customers are waiting to see how the Lenovo deal plays out before making X86 server purchases," Jeffrey Hewitt, research vice president on the Data Center Convergence team at Gartner, told us by email.

It is hard to say for sure if Hewlett-Packard and Dell have been able to benefit from the IBM-Lenovo deal. Some large enterprises keep two system vendors in their datacenters just to instill some competition, so there is probably some of that, but oftentimes these days Cisco's UCS iron is the new alternative server platform sitting beside HP, Dell, and IBM gear. Cisco sold 62,660 machine in the first quarter, and increase of 16.3 percent, but its revenues were up 37 percent to $616.6 million thanks to a richer mix of configurations.

All of the US-based server makers have had more trouble than in past years selling into China, and a bunch of indigenous server makers are doing better as state-back corporations and government agencies are apparently buying more from Chinese companies. Huawei Technologies, which is headquartered in the electronics manufacturing center of the world in Shenzhen (where IBM also has its X86 server factories), had a 61 percent increase in server shipments in the quarter, pushing out 85,919 machines and bringing in $233.2 million in Q1, giving it a number eight ranking by revenues worldwide. Inspur Electronics was right behind at number nine and nearly quadrupled its shipments to 80,929 machines and accounting for $227.3 million in sales. By shipments, Huawei ranks fourth behind IBM, and Inspur is just behind Huawei at number five. Lenovo also grew, with shipments of 64,970 machines (up 53.2 percent) and revenues of just under $128 million (up 61.8 percent).

HP is still the dominant supplier of servers in the world, with $2.89 billion in sales (down 2.3 percent) driven by 534,652 units (down 7.9 percent). Dell rounded out the top five at number two in sales, with just over $2 billion in revenues (down 5.5 percent) and 464,141 shipments (down 10.1 percent).

Those who make their own machines or who have original design manufacturers like Quanta Computer, Synnex, Wiwynn, Jabil Circuit, Foxconn, and a handful of others do it for them continue to represent a larger and larger part of the systems market. By Gartner's reckoning, such DIY/ODM boxes represented 203,061 machines in the first quarter, up 21.4 percent, and drove $525.6 million in sales. This is not as much as you might think, but it is growing fast. It is generally believed that machines aimed at hyperscale datacenters comprise about 20 percent of annual server shipments and will rise to around 40 percent within the next three to five years. Many of these machines are semi-custom machines sold by the tier one players, and many of them are in rack-based form factors.